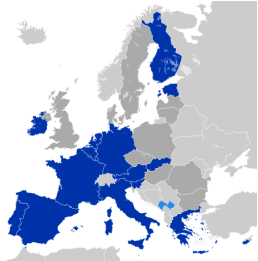

What is the Eurozone?

The Eurozone is a collection of countries in Europe who all use the same currency – the Euro. It came to existence in 1999 with 11 countries opting in, now there are 17 member countries. The Eurozone does not contain all members of the European Union and its monetary rules are controlled by the European Central Bank. The most recent country to join the Eurozone was Estonia in 2011.

The Eurozone is a collection of countries in Europe who all use the same currency – the Euro. It came to existence in 1999 with 11 countries opting in, now there are 17 member countries. The Eurozone does not contain all members of the European Union and its monetary rules are controlled by the European Central Bank. The most recent country to join the Eurozone was Estonia in 2011.

The Eurozone Crisis

The main cause was that the PIGS (Portugal, Italy, Greece, Spain) had lost control of their finances since the global recession – borrowing and spending more than they could realistically afford. Because of this, the other European countries had to bail them out costing billions of dollars. Greece was the first country to accept bailout money in May 2010, followed by Ireland and Portugal. However, this money was doing nothing to help their economies because they were trying to pay off loans, contributing to their debt crises, of a infinitesimal percentage. For these countries, the issue is is that if they have to keep repaying off loans to other countries they could effectively go bankrupt, which could have an even greater adverse effect on Europe, their economy and citizen spending power.

However, before the loans could be approved, the Governments of each of these countries had to agree to adopt ‘austerity measures’ to show they were doing what they can to tackle their economic problems themselves. ‘Austerity measures’ are measures which are taken by government in economic crises in order to cut the budget deficit by using a combination of spending cuts or tax rises. This has led to mass public protests in Greece, with many people demonstrating against more job losses and tax rises as a result.

In the news

Today, there have been increasing issue over the unemployment level which has hit an all time high of 11.8%, meaning that over 26 million people are unemployed across the European Union. The country with the highest unemployment rate is spain at 26.6% unemployed. In the Eurozone alone,unemployment is approximate 18.8 million people – a substantial amount which could prove costly on the economy of Europe.

BBC Economics Correspondent Andrew Walker said: “The general trend of unemployment however remains upwards and it makes it even harder for the governments concerned to collect the taxes they need to stabilise their debts.” The record low for the eurozone unemployment rate was 7.2%, which was recorded in February 2008, before the financial crisis that first gripped the banking sector spread to the real economy. When will the Eurozone reach these levels again?

It has been a bumpy road for the members of the Eurozone and it is a question of what it will take for the economy of Europe to recover fully.

Thanks for reading,

Digestible Politics

The main cause was that the PIGS (Portugal, Italy, Greece, Spain) had lost control of their finances since the global recession – borrowing and spending more than they could realistically afford. Because of this, the other European countries had to bail them out costing billions of dollars. Greece was the first country to accept bailout money in May 2010, followed by Ireland and Portugal. However, this money was doing nothing to help their economies because they were trying to pay off loans, contributing to their debt crises, of a infinitesimal percentage. For these countries, the issue is is that if they have to keep repaying off loans to other countries they could effectively go bankrupt, which could have an even greater adverse effect on Europe, their economy and citizen spending power.

However, before the loans could be approved, the Governments of each of these countries had to agree to adopt ‘austerity measures’ to show they were doing what they can to tackle their economic problems themselves. ‘Austerity measures’ are measures which are taken by government in economic crises in order to cut the budget deficit by using a combination of spending cuts or tax rises. This has led to mass public protests in Greece, with many people demonstrating against more job losses and tax rises as a result.

In the news

Today, there have been increasing issue over the unemployment level which has hit an all time high of 11.8%, meaning that over 26 million people are unemployed across the European Union. The country with the highest unemployment rate is spain at 26.6% unemployed. In the Eurozone alone,unemployment is approximate 18.8 million people – a substantial amount which could prove costly on the economy of Europe.

BBC Economics Correspondent Andrew Walker said: “The general trend of unemployment however remains upwards and it makes it even harder for the governments concerned to collect the taxes they need to stabilise their debts.” The record low for the eurozone unemployment rate was 7.2%, which was recorded in February 2008, before the financial crisis that first gripped the banking sector spread to the real economy. When will the Eurozone reach these levels again?

It has been a bumpy road for the members of the Eurozone and it is a question of what it will take for the economy of Europe to recover fully.

Thanks for reading,

Digestible Politics

RSS Feed

RSS Feed